While shopping online, you must have seen the option of ‘buy-now-pay-later’ as one of the payment options. Today, BNPL is growing rapidly. According to MAG, BNPL lending in the US is forecast to grow significantly over the next 24 months, exceeding $100 billion by 2024.

The BNPL method is quick, easy and convenient as anyone can get a small loan within just a few minutes. It does not require a lengthy registration process. Customers sometimes don’t even have to pay any interest or fees. One of the popular BNPL companies is Affirm. In this blog, we dive deep into the business model of Affirm and analyze its methods through which it generates revenue.

What is Affirm and how it work

Affirm is a fintech company that offers buy-now-pay-later loan services by collaborating with several merchants. When someone is shopping online, they can select the option of Affirm as their payment option. The loan amount can range from anywhere between $50 to $17,500.

If a customer chooses the Affirm’s Buy-now-pay-later option, it will automatically send all the money to the merchant and provide a small loan directly to the customer. While repaying the personal loan, the customer will pay to Affirm, and they will be charged on APRs ranging from 0% to 3%.

Other than APR, Affirm does not charge any additional fee from its customers for account setup, service, prepayment, etc. Unlike a credit card company or loan company which charges customers on basis of compound interest, Affirm charges on the basis of simple interest.

It also does not charge a late fee. If your plan has four biweekly payments or you were only offered one option at the application of a three-month payment term with 0% then it won’t even report it to the credit bureau Experian.

. It gives quick pos loans to customers based on their previous credit score and payment history with Affirm. If your loan is approved, it will provide you with various payment plan options. Customers can repay Affirm in 1-48 months. However, 3-month, 6-month and 12-month payment plans are more common.

Today, Affirm has more than 11,500 merchant partners in various niches, including travel, auto, fashion, etc. It has partnered with leading companies like Walmart, Adidas, Eventbrite, StockX, etc.

How Does Affirm Make Money?

Affirm makes money mainly from two sources. First, it charges interest on the loans it provides to its customers. Second, it charges a processing fee from its partnered merchants for every transaction. However, Affirm has been diversifying its sources of revenue, and it also makes money through interchange fees, sales of loans and loan servicing.

Interest rates

Affirm generates money on interest rates the customers pay for the loans it offers. It is pertinent to note that Affirm does not charge any hidden fees. Anyone can make an Affirm account and get a small personal loan easily.

The APR rates range from 0 APR to 30 APR. The average loan size of Affirm is estimated at around $750. It claims that customers usually repay the loan within nine months at an APR of 18 per cent.

Affirm underwires all its loans via Cross River Bank, Celtic Bank or Affirm Loan Services, which allows it to make higher volumes of loans and better margin rates.

Affirm has an AI algorithm that assesses credit risk associated with all the customers before providing them with a loan. It considers factors like credit score, payment history with Affirm, duration of the customer’s relationship with Affirm, credit card debt, interest rate offered by merchants, income, etc.

Merchant Fees

Affirm also charges fees from its partnered merchants for every sale via its platform. The company has not publicly revealed its fee structure, but it is estimated to be 2 percent to 3 percent. The merchant fee depends upon factors like sales volume, purchasing price and the types of goods sold.

The merchants pay a fee to Affirm for managing the payment process and taking on the risk of a payment default. Moreover, Affirm claims that patterning with it will help merchants to increase their sales order volume by 85% and there will be at least a 20% increase in repeat orders.

Interchange Fees

In late 2021, Affirm started issuing debit cards to its customers by partnering with payment processor company Visa. There were more than one million people on the waiting list before the launch. Henceforth, Affirm also generates revenue through interchange fees.

The interchange fee is paid by the merchant who accepts that payment. Visa charges around 1.14 percent to 2.4 percent. Affirm, and Visa has not yet disclosed the revenue-sharing agreement between them.

Sale of Loans

Affirm sells a small portion of the loans from the originating bank partners to third-party investors. It makes money on such loans by earning the profit between the proceeds received at the date of sale and the loan’s carrying value. Its banking partners include Cross River Bank and Celtic Bank.

Loan Servicing

Affirm also makes money by providing professional financial services to manage loan and debt portfolios on behalf of its third-party owners. Loan servicing contributes almost 2-3% of the total revenue of Affirm.

How much money did Affirm make?

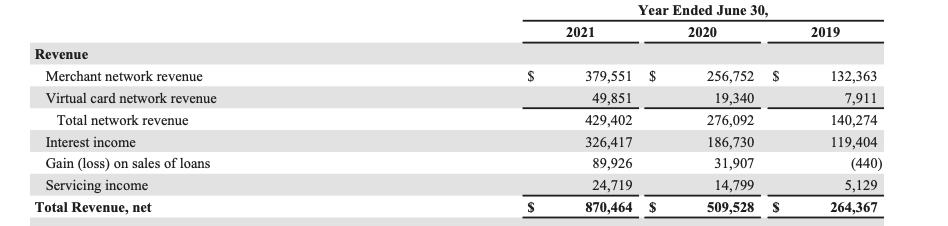

(Source: Affirm’s Annual Report)

There are two primary sources of income for Affirm: Merchant Network revenue and Interest income. It generated $379.5 million or 44% of its revenue from merchant fees and $326.4 million or 37% from interest.

Affirm is trying to diversify its financial services by bringing in debit cards. It contributed 6 per cent to its total revenue in the fiscal year 2021. It generated $89.9 million, or 10% of its revenue from the sale of loans. Also, the company generated $24.7 million or 3% of its revenue from service fees.

Affirm is also trying to expand itself. In 2021, it acquired Returnly, a firm that helped consumers return their products. It is also growing its merchant network and now, Shopify has become its merchant partner. It has struck a deal with it for Shop Pay Installments. This move helped Affirm to expand its number of merchant partners and consumers significantly.

It has even launched its designated shopping app, Super, in early 2022. It is a one-stop destination for all shopping needs and helps customers to manage their finances effectively.

Affirms history

Headquartered in San Francisco, Affirm was founded by Max Levchin, a former PayPal co-founder, in 2012. It is a fintech company that offers buy-now-pay-later service at point-of-sale to consumers. As of 2021, it has more than 11 million customers in the US and Canada and over 170000 merchant partners.

Max Lechin was born in Kyiv, Ukraine. Since his childhood, he was always keen on computers and coding. Soon, his family migrated to the United States, where he pursued a Computer Science degree from the University of Illinois.

He was always passionate about entrepreneurship during his college days and had three businesses. One was NetMeridian, a software tool he later sold to Microsoft for $100000 before his graduation. Later, he started working on his new venture with his other University friends and that venture, PayPal, created a revolution in the online payments sector.

However, in 2002, PayPal was acquired by eBay for an estimated $1.5 billion. Levchin, who was PayPal’s CTO, got $34 million out of that deal. Soon after, he started Slide, a social media app like Facebook or Instagram, but that was sold to Google in 2010 for over $180 million. Then, he worked with Google for over a year. But soon left it, to start Affirm.

Initially, Levinchin decided only to be the chairman and investor of Affirm. Still, afterwards, he became so consumed and fascinated with the idea of Affirm that he decided to take full leadership. Today, he is the CEO and the founder of Affirm.

Funding and Valuation

Affirm went public in January 2021 with a list price of $49 and raised $1.2 billion with a valuation of $11.9 billion. On the first day, shares traded at $90.90, and by mid-afternoon, the price rose to over $100. In February, the value of the stock rose to $125. However, it did not perform well after that and went as low as $53 in May. Then it rose again to a whopping $176.6 per share in November 2021.

Then again, in 2022, the share price started falling. In February 2022, the company accidentally disclosed their second-quarter earnings on Twitter. It reported a loss of $160 million for Q2. This event affected its share price, and as of now (June 2022), it is trading at $20, quite below its IPO list price.

Earlier it had notable investors like Spark Capital, Wellington Management, Founders Fund, Lightspeed Venture Partners, Khosla Ventures, Andreessen Horowitz, and many others.

Affirms Competitors

Let’s look at the top 5 competitors of Affirm:

Afterpay

Afterpay is a ‘buy now, pay later (BNPL) platform that offers short-term financing loans to its customers without any interest. Its customer base is in Australia, New Zealand, the United States and Canada. It is also available in countries including UK, France and Spain, where it is known as Clearpay. It is now acquired by the digital payments company Block.

Sezzel

Sezzle was founded in 2016 and is one of the top players in the BNPL industry. It allows customers to pay back in small four-month installment payments with no interest rate. In 2020, it even launched a virtual debit card similar to that of Affirm virtual cards. As of now, Sezzle has over 7.8 million user sign-ups and 40000 merchant partners.

Also Read: How Many Downloads Does Fortnite Have?

PayPal Credit

PayPal Credit gives its users an option of an extended period to pay for certain purchases by assessing their credit history. One can choose the PayPal credit option while checking out of the cart in online stores and retailers that accept PayPal.

Klarna

Klarna is a ‘buy now, pay later’ Swedish company founded in 2005. It is available in more than 20 countries and is used by 90 million shoppers worldwide. Klarna has partnered both with online as well as in-store merchants. It will do a soft credit check before giving out any loans. It has partnered with popular brands like Apple, Macy’s, Foot Locker, and Sephora, allowing customers to make small payments on big-ticket goods.

Splitit

Splitit is a “responsible” BNPL service provider company. It lets customers make interest-free monthly payments on their online purchases. They do not have to bear any additional registration or application fee. It has partnered with retailers like Avery and SofaClub.